Westpac Ups The Ante On Scam Protection

- 18.11.2024 11:30 am

WorldFirst Partners With Walmart for Secure Online...

- 07.08.2024 01:05 pm

Klickl Taps Sumsub for Enhanced Compliance, Fraud...

- 31.07.2024 01:15 pm

Inferior database security led to the downfall of...

- 21.02.2024 09:51 am

24/04 – Weekly Fintech Recap

- 24.04.2023 09:00 am

11/11 – Weekly Fintech Recap

- 11.11.2022 06:00 pm

Equals Group Partners with Featurespace to Enhance...

- 22.08.2022 10:55 am

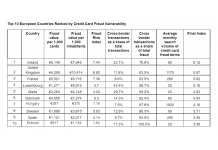

New Research Reveals Ireland is the Credit Card Fraud...

- 01.08.2022 09:50 am

18/07 – Weekly Fintech Recap

- 18.07.2022 09:00 am

Red Hat Releases Open Source StackRox to the Community

- 17.05.2022 01:25 pm

MSAB Part of New European Standard for Mobile Forensics

- 05.05.2022 09:20 am

Vyta Receives £11M Investment from MML and Acquires IT...

- 04.05.2022 11:10 am